How to Evaluate Longevity Stocks

Looking back on market-wide trends is to look back at the course of ships past sailed. Hindsight is 20/20, and the investment market is chock-full of missed opportunities. Amazon in 1997, Google in 2004, Bitcoin in 2017, and NFTs in early 2021 – the list goes on. Who knew that the stock market would go on a massive bull run following the epic crash and brief bear market in February 2020?

Trying to catch the next windfall is equally as frustrating as looking back at the “one (or ones) that got away.” Will crypto make a resurgence? Are DAOs the next revolution in managing company equity and voting rights? Is the Metaverse doomed to fall short of Neal Stephenson’s Snow Crash projection or just a few years ahead of widespread adoption?

Nothing is a sure bet, but there is one thing that’s a near guarantee:

- National health expenditures will continue to rise by around 5% annually

- Healthcare will comprise nearly 20% of America’s GDP by 2030.

Traditionally, healthcare stocks are a haven for value investors.

But what about the younger or more risk-seeking population? Is there an option within healthcare that can potentially provide outsized gains that takes advantage of new and growing trends?

The fast-growing longevity biotech sector might be the answer.

Many investors may balk when they hear “biotech” and “investing” in the same sentence…

Long clinical lead times, regulation, and incomprehensible scientific jargon make the longevity biotech industry much more difficult to wrap your head around than most investments. But, the smart money is starting to see something in aging research and the biotech firms involved.

The groundbreaking therapeutics and science behind these companies stand the chance to change biotech and the world of healthcare as we know it. In the process, of course, this gives early investors the opportunity for substantial returns.

That said, perhaps it’s time to take a more reasoned look at the securities available today, the risks involved, and the optimal approach for any investor looking to gain exposure.

Leveraging Longevity

The longevity sector consists of individual firms that may focus on:

- Blunting, slowing, or reversing the effects of aging through medical applications

- Increasing lifespan via intervention throughout each life stage

- Transhuman-style technological implants and interfaces to achieve longevity goals (this is generally on the more ambitious side of current longevity research)

Many of these firms’ missions, goals, and technologies are highly technical and stuffed with medical jargon, further emphasizing the need for either exhaustive due diligence or expertise in the field when evaluating a company’s potential.

A prospective investor may feel the need to know the difference between a firm developing monoclonal antibodies to target protein growth factors and a firm treating systemic inflammation through allogeneic cellular medicine that’s developing mesenchymal lineage adult stem cells.

All Greek to you?

Don’t worry; this post will highlight why it may not even be necessary to focus specifically on the technical aspects of the longevity market – not at this stage, at least.

Evaluation and Valuation

There’s one significant difference that sets biotech investing apart from investing in, say, companies that make up the S&P500.

Typical investors hold stock in a company for the promise of a return of future cash flow via dividends or mergers and acquisitions. This is simplified and doesn’t account for the many other reasons people might invest, but that is the underlying principle of investing.

However, biotech firms are often financially unstable and cannot return equity to shareholders through dividends. What is the draw, then?

The looming potential – AKA, growth.

When Gilead (GILD) went public in 1992 it wasn’t clear that the stock was going to be one of the largest biotech success stories, currently returning more than 11,000% since IPO.

Biotech investors generally approach the market in hopes to see those types of gains. And although the quest to find another Gilead is difficult, it’s certainly not impossible.

So how does it all shake out? And where do you even begin?

Qualitative Quandary

When evaluating a longevity biotech firm, a qualitative assessment is a layperson’s first and most challenging step. This looks at the quality of the company’s product, the viability of the technology, and variables such as the likelihood of FDA drug approval.

Probably the most important qualitative metric when looking at biotech companies’ value is their probability of FDA approval. Unlike most other industries where value is driven by sales, users, profits, and other growth metrics, the biotech industry’s value is largely derived from how close the companies’ treatments are to becoming FDA-approved.

To interpret FDA phasing, you need to understand how the process works:

- Phase 1: 20-100 volunteers; several months of testing. 70% of drugs move forward to the next phase.

- Phase 2: Several hundred subjects; up to two years of testing. 33% of drugs move to Phase 3.

- Phase 3: 300 – 3,000 patients; 1-4 years. 25-30% of drugs move to the final phase.

- Phase 4: Several thousand volunteers; several years

Following Phase 4, the drug moves to final FDA approval, which can take up to 10 months for a decision – and approval isn’t guaranteed.

Each consecutive phase requires more investment from the company, but also results in more value. A failure at any phase generally results in the value dropping to $0.

Without a biomedical engineering degree, it may be difficult for a non-professional investor to analyze these qualitative measures.

Other qualitative metrics can serve as a stand-in, including the number of patents filed (generally, the more, the better), experienced management teams, etc.

In general, the qualitative assessment of biotech and longevity firms is challenging, exhausting, and rapidly changing as developments arise.

But if you think the challenges stop there, hold on to your hats…

Quantitative Qualifiers

Another way to evaluate biotech firms is through financial or quantitative analysis. It’s another difficult process because many relied-upon financial multiples and metrics used to assess broad market stocks don’t necessarily work with biotech because of the inherent unprofitability of early-stage, pre-development firms.

Even though they may have gone public to raise funding, they are, in many ways, still startups, and their financials typically reflect that status.

The sections below will look at how this plays out in the real world. For now, just remember that standard financial metrics like price-earnings (P/E) ratio, cash flow, earnings, etc. may not reflect the potential value of a longevity biotech firm as they do with traditional companies.

That said, here’s what you should look at when evaluating your typical small-cap longevity stock:

- Runway. This cash flow metric measures how long the firm can operate at current levels before it exhausts its cash reserves or needs further funding. Since these companies likely aren’t generating a profit, we must keep a close eye on how long they can operate without running out of cash.

- Burn Rate. This is a critical component of the runway and is how much cash is spent in a period. This, coupled with cash flow projections and the size of the company’s war chest, tells you how long the company can keep up these cash burn levels – or the runway.

- Path to profitability. Also known as the P2P, this is a symbolic road parallel to the runway that lays out, by milestone or period, the steps, requirements, and length of time necessary before the firm is profitable.

- Drug pipeline. A non-financial metric, the drug pipeline is the queue and status of each drug or proprietary technology a firm has currently under development. The pipeline can refer to internal progress or where it stands concerning approval and rollout.

A standard measure for determining valuation is the discounted cash flow (DCF) model, which can be applied to biotech firms with some modifications.

DCF modeling is, even in its most basic form, more of an art than science, and this is especially true for biotech. Biotech DCF models assign a projected cash flow to each drug or tech through research into the market potential and planned pricing of the product, among other variables.

The model also determines the drug pipeline progress and overlays the two alongside other variables to project financial wellness.

Analysis Example: Geron Corporation (GERN)

Now let’s apply these measures to a real-world example. In a sense, this is us walking you through how one would evaluate an individual longevity biotech stock.

While it is subject to change over time, Geron Corporation is currently weighted at 7% in our index.

To start, let’s take a qualitative look at what Geron is working on.

For future commercial use, Geron is developing a telomerase inhibitor called Imetelstat.

Without going into extreme detail, telomeres are caps of DNA on chromosomes and protect the chromosome from damage. Telomeres shorten with age, and the prevention of shortening or “fraying” of telomeres is a goal of many longevity firms.

Telomerase is a protein that “tells” telomeres to restore themselves after cell division, maintaining the integrity of the chromosome after splitting and allowing cell division to continue. Without telomerase, cell division would stop after reaching a limit encoded in the cell.

In normal circumstances, telomerase is present and aids ongoing cell division in:

- In-utero fetal tissue; helps ongoing cell division to “build” the baby.

- Skin cells; aids tissue repair.

- White blood cells; help regenerate the cells and maintain the body’s immune system.

In abnormal circumstances, telomerase contributes to the rapid spread of cancer. Some cancer cells exhibit telomerase activity, allowing for infinite division and expansion. This leads to rapid spreading throughout the body.

Geron is developing a telomerase inhibitor, a commercial application being used to treat cancer. Reading between the lines (since we know that telomere shortening and fraying goes along with aging), it isn’t a stretch to assume that secondary and tertiary research could result in direct longevity breakthroughs.

Now, let’s take a look at the company’s standard financials and attempt to evaluate them from a quantitative perspective.

At the time of writing, Geron has:

- An earnings-per-share (EPS) of $-0.36

- A 594 price-to-sales (P/S) ratio

- -79% return-on-equity (ROE)

- -51% return-on-assets (ROA)

Financial analysts may use this data to point to a series of red flags, but there are also some silver linings in the financials:

- A 0.9 beta, which means that it is less volatile than the broad market – i.e. if the S&P500 moves up or down 1%, then Geron moves 0.9%.

- Institutions hold 48% of the company equity, and short (those who are betting against the stock) interest is less than 5%. These two combine to tell us that the smart money thinks Geron is viable for future potential.

After a brief look at standard financials, we can now look at the biotech-specific valuation measures.

By analyzing Geron’s 2021 annual report, we see:

Cash Measures

At the end of 2021, Geron had $187M in cash or cash equivalents on its balance sheet. Their cash burn over the preceding year was $40.5M giving Geron a runway of 4.6 years at its current pace with no more financing.

This good news is somewhat offset by Geron’s debt assumption over the year – the firm took on $24.9M in long-term debt.

Long-term debt, for one, is never a great thing. It also poses risks to shareholders because debtors get paid first in the event of a liquidation. Even pre-IPO investors could see their initial capital disappear.

An alternative to total debt is a look at the debt-to-equity (D/E) ratio, where the lower the ratio, the better. For context, Geron has a D/E ratio of .51 compared to the biotech industry average of .27.

Path to Profitability (P2P)

Geron’s path to profitability is difficult to determine because these assessments are often guarded secrets. In the case of a small-cap biotech stock with no commercial distribution and only drugs in the pipeline, the only real way to measure future profitability is to estimate the market potential of its specific drug candidates, the costs associated, FDA approval probabilities, and the competitive landscape.

While there are certain financial connoisseurs who do track P2Ps for selective biotech firms, for the purpose of this exercise, we’ll just skip ahead.

Drug Pipeline

Geron has two drugs mid-way through Phase 3, with one (IMerge) closed to enrollment and the other (IMpactMF) open for enrollment. We can then estimate that these drugs are anywhere from 2-4 years until entry into Phase 4 (if they move on).

Even in a perfect scenario, we’re looking at roughly 5-10 years until FDA approval and commercial distribution.

So, now that we’ve done (mostly) all the homework… What does it all mean?

While this is not investment advice, the company looks strong financially compared to the industry norms, but the extended drug candidate timeline is concerning.

Even though ten years’ time may yield successful returns after commercialization, you’re practically holding money in a stock that will likely trade flat during that time frame (although there will certainly be many ups and downs from quarterly news/earnings).

So, is Geron Corporation a sound stock?

To be brutally honest, it’s still hard to tell.

Defining Risk

Simply put, any time you are at the cutting edge of technology or science, it is difficult to value the companies involved. That’s why, although there is plenty of money to be made investing at such an early stage, we need to take a quick look at risk and how it’s applied to the biotech market

There are two broad risk types in investing: systematic and idiosyncratic.

Systematic risk is a risk to the market, industry, or economy – think COVID-19, the Great Recession, or the Dot-Com bubble. Systematic risk is technically diversifiable through alternative investing strategies. But for our purposes, we’ll assume that systematic risk = undiversifiable risk.

This leaves us with idiosyncratic risk, which is diversifiable. This risk category is specific to a company and can arise from many factors like mismanagement, product recalls, etc.

In biotech and longevity firms, idiosyncratic risk is exceptionally high. That’s because a company’s livelihood and future are tied to regulations and ongoing clinical trials. In other words, years of company progress can be swiftly undone due to any factor of negative things.

The undue risk in individual companies establishes the need to diversify rather than going all-in on one or two particular stocks.

Diversification

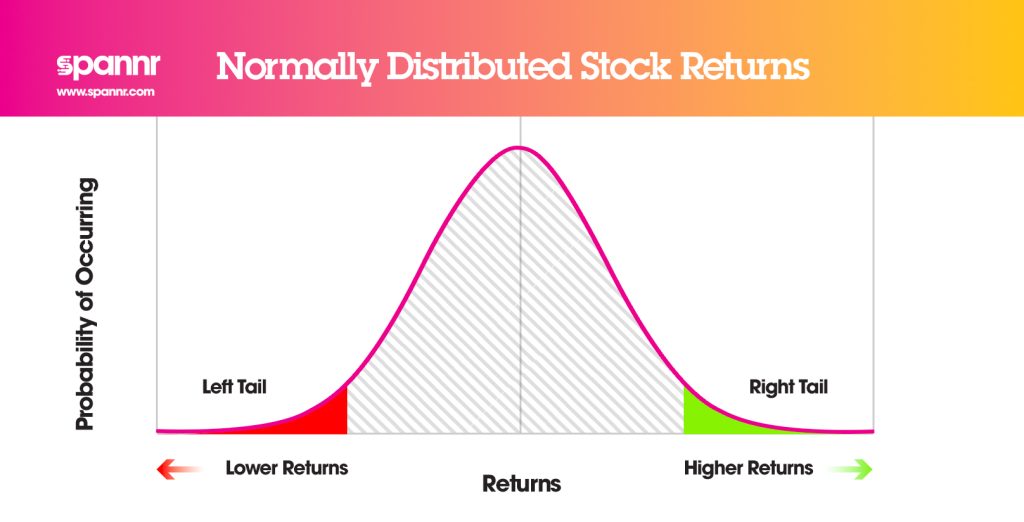

Over time, stocks in an index tend to gather around a mean return – a standard distribution. The best way to visualize this is by plotting returns on an x-axis and drawing a bell curve.

That’s to say that in any given market, no matter an individual company’s return or volatility, the bulk of returns gravitate towards the center of the bell curve.

Using the average market as an example, an investor may make comparatively outsized returns in one year, like +28% in 2021, and excessive losses in another, like -38.49% in 2008. But over time, their return normalizes (historically around 10%), as long as they continue to hold. Pretty basic, right?

Here’s where it gets crazy though.

Although the average return of a market will tend to be around the center of the bell curve, less probable returns will also occur in the “tails” of the curve. These less probable returns (both positive and negative) are where the bulk of annualized investment returns actually come from.

In basic terms, this means that if you were to cherry pick a company in any given market, say longevity, you would have the potential to accidentally choose what JPMorgan calls a “megawinner,” or a company that strikes big and keeps their momentum moving – think Google, Amazon, etc.

But you would just as likely pick a company that would lead to lower returns than the average market – potentially even losing it all.

What does this teach us? The importance of diversification.

Suppose you hold a basket of longevity stocks instead of just one or two. In this case, you can capture the right-side tails, or the massive outperformers (which we believe there will be a lot of in this market). At the same time, you are also mitigating the left-side tails that would otherwise destroy your net worth.

By holding a large basket of biotech stocks, you can also diversify phasing and timing alongside risk.

Think about it – if ten stocks are in various phases of clinical progression, you’ll see returns in a phased manner as they move through the system. This will let you generate returns while also holding the longer-term assets for future potential.

Diversifying is always vital but especially relevant in an industry like biotech and longevity – think of it as casting a wide net to catch as many fish as possible.

Putting It All Together

Unless you have a crystal ball of some sort, cherry-picking individual longevity biotech stocks is a difficult task to say the least.

As we saw with the Geron (GERN) example above, it’s nearly impossible to know exactly how the company will pan out in the years to come.

That said, your best chance for substantial returns as a longevity biotech investor is to throw pretty much everything you think you know about investing out the door.

Qualitative analysis?

Forget about it.

Quantitative analysis?

Forget about it.

Expert clinical analysis?

That too.

The trick is to practice patience, and to diversify.

Functionally, this is how venture capitalists and private equity firms invest.

They know that maybe two or three investments will return their capital plus some appreciation. Many others will collapse and maybe return their money. But those megawinners are the ones that define the VC fund.

For an analog, look at Peter Thiel, the renowned venture capitalist and angel investor who has invested in dozens of firms. His early $500,000 investment in Facebook gained hundreds of millions of dollars in returns, offsetting losses and marginal performance from other investments.

What else is critically important when gaining exposure to these early-stage longevity stocks?

Mindset.

In longevity biotech, many companies will make bold claims and publish flashy press releases, only to have nothing substantive behind them besides a pile of burned shareholder equity once the jig’s up.

Falling prey to these schemes is a hallmark of the “get rich quick” mindset that rarely produces consistent results. If it sounds too good to be true, it probably is.

Putting it all together, you want to have a portfolio that consists of all the companies that have a legitimate shot at being a megawinner in the longevity biotech industry.

It’s perhaps a good reason to invest alongside a longevity biotech fund or index.

About the Author